Pensions can be a daunting topic for employers. As one of the costliest and administrative-heavy parts of employee remuneration, it’s no wonder that most organisations try to leave it relatively untouched and automatic. Unfortunately, not taking a deep look into how to improve and optimise your pensions can lead to a build-up of invisible costs and missed opportunities for savings. In this article, we outline one of the best ways employers can optimise their pensions and make employees happier.

Introduction to salary sacrifice pension

Salary sacrifice pension is an agreement between you and your employees. Employees can give up part of their future gross salary or bonus in return for a non-cash benefit, like a pension contribution.

With the reduction of cash pay, both employers and employees can save on National Insurance contributions and income tax, becoming more tax-efficient. The NI and tax savings can then be used to boost pension pots and increase their value over time. Ultimately, this system allows employees to make the same amount of contributions for a lower cost, or a higher level of contributions for the same overall cost.

It really is a win-win, which is why, according to Willis Towers Watson, 86% of the FTSE 350 use it.

Why should employers use this scheme?

You probably already know this, but there is a lot of money going into National Insurance Contributions. The higher the salary of your employee, the more you have to pay. Even if your employee’s earnings are not too costly, those numbers quickly add up as your team expands.

In return for accepting a lower salary, the employee no longer makes their own contributions into the pension scheme. Instead, the employer makes contributions into the scheme that are equal to the amount of the contributions that the employee was previously making of which is not subject to NICs.

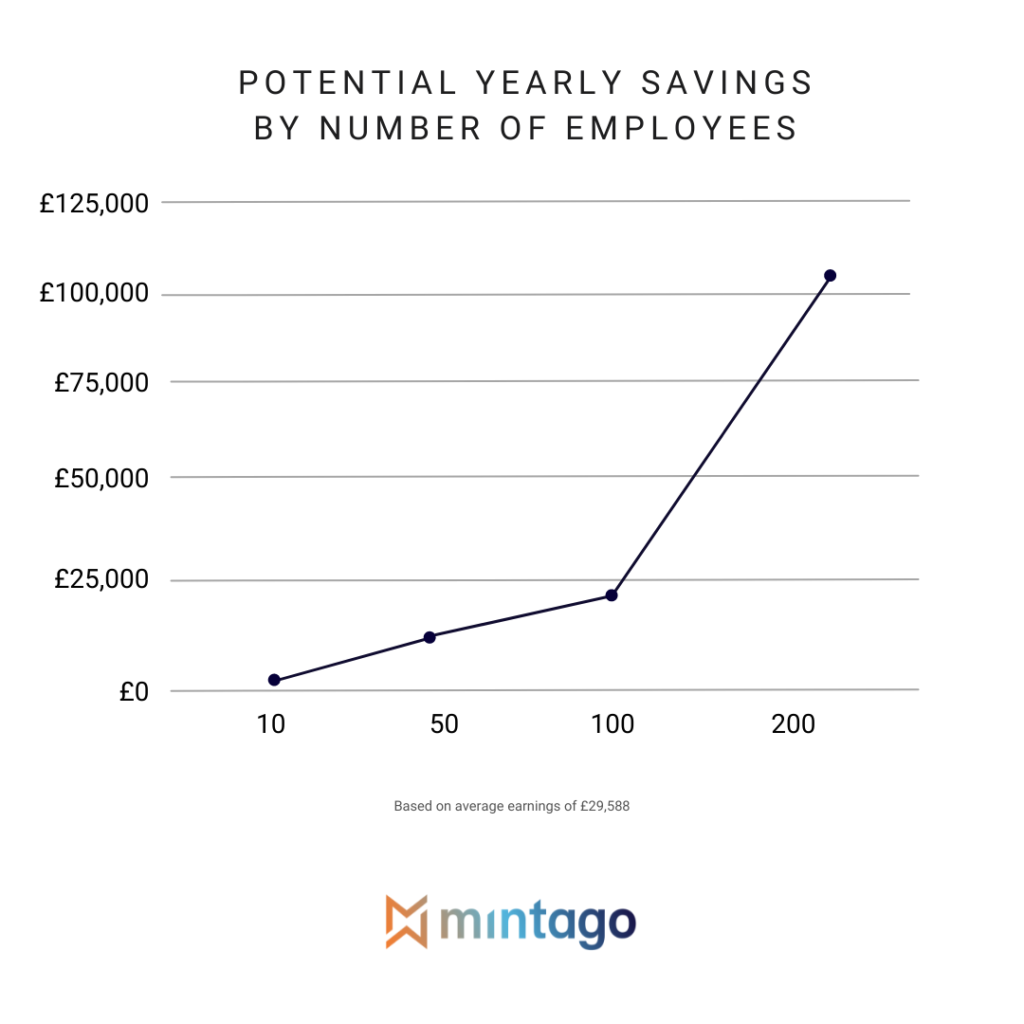

Ultimately, reducing overall salaries across a large workforce can achieve substantial savings. Employers can save up to 13.8% of the amount paid by the employee to their pension. Let’s look at that in numbers

Implementing Salary Sacrifice can also generate a more attractive benefit package for employees.

With the majority of the workforce now considered Millennials, workplace perks and an emphasis on work/life balance through benefits is becoming more important than ever.

The tax-free benefits include:

- Employer-provided pensions advice

- Workplace nurseries

- Childcare vouchers and directly contracted employer-provided childcare that started on or before 4 October 2018

- Bicycles and cycling safety equipment (including cycle to work)

- Season ticket loans

You can also choose to reinvest part of the company’s NI savings back into your team – increasing their wellbeing budget, adopting new tech, creating work from home stipends…there are loads of exciting schemes to choose from.

This sounds too good to be true. Why would employees opt into this scheme?

Employees might be weary at first to agree on a salary reduction. However, the benefit received as a result of the sacrifice and the reduction in salary will easily cancel each other out.

Not only do employers pay less NICs, but so do employees. This means they can save up to 12% of the amount they pay into their pension as a personal contribution:

Furthermore, reducing salaries can also help employees in specific circumstances. Employees that earn just over the £50,000 threshold can cut their wages to less than that amount so as to continue to receive benefits from the government, like child benefits. Salary sacrifice can also help members of your team looking to delay repaying student loans.

Ultimately, employees just need to be kept well-informed about all aspects of salary sacrifice and how it will impact their before and after implementation.

FAQs on Salary Sacrifice

Is this tax avoidance?

Not at all! The Salary Sacrifice scheme is 100% backed by the HMRC:

Salary sacrifice is commonly used by employers or employees to take advantage of the exemption from tax or NIC or both of certain benefits. It is important to recognise that employers and employees have the right to arrange the terms and conditions of their employment and to enjoy the statutory tax and NIC treatment that applies to each element in the remuneration package. Arrangements, which are designed to make use of these exemptions, should not be regarded as avoidance.

How much salary can be reduced?

It’s ultimately under the discretion of your employee how much of their salary they’d like to sacrifice. However, the law requires that Salary Sacrifice arrangements must not reduce an employee’s earnings below the national minimum wage rates.

Is salary sacrifice pension suitable for everyone?

There’s rarely a one-size-fits-all plan for staff. Salary Sacrifice works because it is a mutual agreement between employer and employee, allowing employees to have a careful think whether it makes sense for their circumstances and future goals. Usually, this is most attractive to higher-earners in the organisation.

What are the risks of Salary Sacrifice?

Most employees will benefit to receive extra pension contributions, but a handful might choose to opt out if they are looking to borrow for a mortgage in the near future or have other outstanding needs that require a full paycheque.

Salary sacrifice can affect an employee’s entitlement to earnings related benefits such as Maternity Allowance, Additional State Pension and Life Cover. It may also affect an employee’s entitlement to contribution based benefits such as Universal Credit and State Pension. It may reduce the cash earnings on which National Insurance contributions are charged. However, an employee might be able to claim more tax credits.

How do we get started on the scheme?

It’s important that an arrangement is documented in writing as it technically constitutes a change to the original contract of employment. Although it’s no longer required to report Salary Sacrifice cases to HMRC, they could ask for copies of formal documentation at a later date. Employers must consult with their employees over changes in their contract and pension schemes.